El "Libro Blanco sobre la Exportación de Dispositivos Médicos Chinos al Sudeste Asiático" presenta principalmente la situación relacionada con la exportación de dispositivos médicos chinos al Sudeste Asiático, incluyendo el desarrollo industrial, la tendencia de las exportaciones, la situación macro de los países del Sudeste Asiático, las oportunidades en la industria médica y de dispositivos médicos, el marco regulatorio de registro, las rutas de exportación y las regulaciones de cada país, con el objetivo de proporcionar una referencia para las empresas chinas de dispositivos médicos que se expanden al extranjero.

1. Desarrollo de la industria de dispositivos médicos chinos y tendencia de exportación

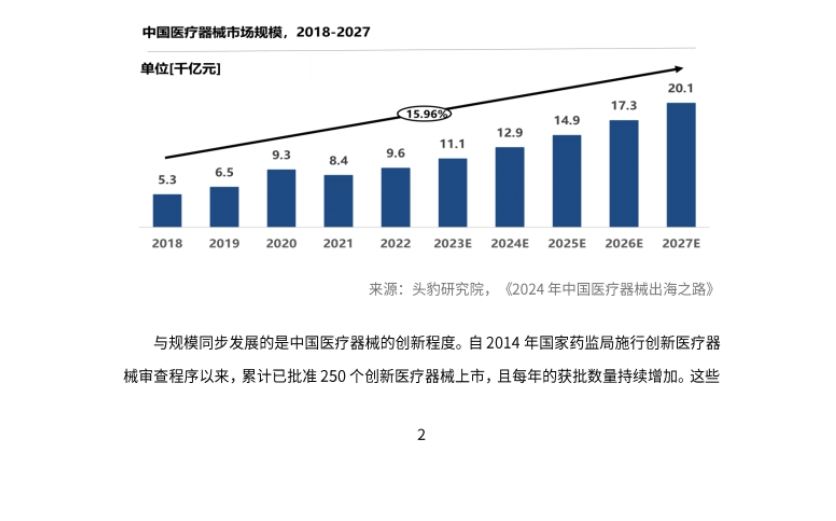

- Crecimiento del mercado e innovación: El mercado global de dispositivos médicos crece de manera constante, y el mercado chino se desarrolla rápidamente, alcanzando ya el 25% del mercado global, con una proyección del 44% para 2027. La capacidad de innovación de los dispositivos médicos chinos sigue avanzando; desde 2014, se han aprobado acumulativamente 250 dispositivos médicos innovadores para su comercialización, de los cuales el 77% son de fabricación nacional.

- Situación general de las exportaciones: La demanda de exportación de dispositivos médicos chinos es amplia. El valor de las exportaciones creció rápidamente durante la pandemia de COVID-19, las categorías de productos se han enriquecido gradualmente y la competitividad en el extranjero ha mejorado. La proporción de ingresos en el extranjero de las empresas de dispositivos médicos que cotizan en bolsa en China aumentó del 24% en 2017 al 38.8% en 2021, cayendo al 34.9% en 2022, siendo los consumibles de bajo valor el núcleo de las exportaciones.

- Exportaciones a países de la ASEAN: La ASEAN es el tercer mercado de exportación más grande para productos farmacéuticos y de salud chinos, y las exportaciones de dispositivos médicos chinos a la ASEAN representan una proporción significativa. En 2022, las exportaciones a la ASEAN fueron de 13.68 mil millones de dólares, en 2023 de 11.3 mil millones de dólares, y en el primer semestre de 2024, las exportaciones alcanzaron los 5.869 mil millones de dólares, un aumento interanual del 2.64%, de los cuales las exportaciones de dispositivos médicos fueron de 2.628 mil millones de dólares, un aumento interanual del 1.12%. Países como Vietnam y Tailandia lideran en la proporción de exportaciones en el mercado de la ASEAN.

2. Introducción macro de los principales países del Sudeste Asiático y análisis de oportunidades en la industria médica

- Situación macro general

- Crecimiento del PIB y del PIB per cápita: Las economías de los países del Sudeste Asiático crecen rápidamente, con una buena recuperación post-pandemia y un crecimiento del PIB superior al de China. El PIB total en 2022 fue de 3.6 billones de dólares, con una proyección de 5.5 billones de dólares para 2028, y el PIB per cápita alcanzó los 5,500 dólares en 2022.

- Características demográficas y estructurales: Gran población, expansión de la clase media, estructura poblacional joven pero con un envejecimiento acelerado. La población total en 2022 fue de 680 millones de personas, y el envejecimiento en algunos países se agrava, lo que aumentará la demanda de atención médica.

- Gasto en salud: El gasto per cápita en salud y su proporción del PIB han aumentado, pero aún hay margen de crecimiento en comparación con los países desarrollados. La tasa de crecimiento anual compuesta del gasto per cápita en salud entre 2000 y 2019 fue del 9%.

- Oportunidades de exportación para la industria de dispositivos médicos chinos

- Énfasis gubernamental en la inversión en salud: Los gobiernos de los países del Sudeste Asiático han priorizado la construcción del sector salud después de la pandemia, como el aumento del presupuesto del Ministerio de Salud de Malasia, y los países prestan atención al desarrollo de la informatización hospitalaria, la telemedicina y el turismo médico.

- Dependencia de las importaciones de productos médicos: La industria manufacturera local de productos médicos en el Sudeste Asiático es débil, y la mayoría de los dispositivos médicos dependen de las importaciones, como en Singapur y Malasia, donde la proporción de importaciones es alta.

- Políticas favorables de cooperación económica y comercial: La cooperación económica y comercial entre China y la ASEAN es profunda, con un buen entorno político, como el avance continuo de la construcción de zonas de libre comercio, la entrada en vigor del RCEP que reduce los riesgos políticos, y la cooperación en múltiples áreas.

3. Introducción a la industria médica y de dispositivos médicos en los principales países del Sudeste Asiático

- Resumen: PricewaterhouseCoopers clasifica los mercados médicos de los países del Sudeste Asiático en mercados primarios, emergentes y maduros, con diferentes características. Fitch Ratings pronostica las tasas de crecimiento anual compuesto del mercado de dispositivos médicos de cada país, como Indonesia con un 10.8%, Vietnam con un 10.2%, etc.

- Discusión por país

- Singapur: Alto gasto en salud, alta calidad de servicio, envejecimiento poblacional severo, creciente demanda de telemedicina y atención domiciliaria. La industria de dispositivos médicos se desarrolla rápidamente, con alta dependencia de importaciones, más del 80% de la demanda se satisface con importaciones, y se espera que las importaciones crezcan aproximadamente un 7.0%.

- Malasia: Sistema de prestación de servicios de salud diverso, enfoque en la prevención y tratamiento de enfermedades no transmisibles y cuidado de ancianos, muchas oportunidades de investigación clínica. Cuenta con muchos fabricantes de dispositivos médicos, lidera en exportaciones de productos de gama baja, pero depende de importaciones para equipos de alta gama, con una proporción de importaciones del 88%.

- Tailandia: Turismo médico desarrollado, envejecimiento poblacional, creciente demanda de equipos médicos de alta tecnología. El mercado de dispositivos médicos es grande pero con baja autosuficiencia, el 90% depende de importaciones, y los equipos chinos representan la mayor proporción del valor total de las importaciones.

- Indonesia: El gobierno prioriza la construcción médica, integración de hospitales estatales, envejecimiento poblacional, enfrentando una crisis de enfermedades no transmisibles. El mercado de dispositivos médicos crece rápidamente, con una tasa de crecimiento anual compuesta del 10.8% entre 2021 y 2026, pero las políticas proteccionistas del gobierno afectan las importaciones.

- Vietnam: Transformación del sistema de salud, aumento del gasto, envejecimiento poblacional, desafíos para hospitales públicos y privados, fomento de la importación de equipos médicos con aranceles bajos y sin restricciones de cuotas. Más del 90% de los dispositivos médicos dependen de importaciones, con una tasa de crecimiento anual del 9.7% entre 2021 y 2026.

- Filipinas: El sistema de atención médica está compuesto por sectores público y privado, con cobertura universal de seguro médico, turismo médico emergente, y muchas oportunidades en el mercado de TI de salud y dispositivos médicos innovadores. Alta dependencia de importaciones de dispositivos médicos, la producción local se limita a equipos básicos y artículos desechables, con una proporción de importaciones del 99.2%.

4. Marco regulatorio de registro de dispositivos médicos en países del Sudeste Asiático y resumen

- Introducción a la Directiva de Dispositivos Médicos de la ASEAN (AMDD): Implementada en 2015, busca armonizar la regulación, incluyendo principios básicos, documentación técnica de dispositivos médicos, clasificación, etc., mejorando la consistencia en los estándares de registro y supervisión.

- Resumen de la regulación de registro de dispositivos médicos en los principales países del Sudeste Asiático: Existen diferencias entre países en clasificación de dispositivos médicos, materiales de solicitud, plazos de registro, etc. El informe presenta los requisitos básicos de registro de los principales países, tomando Singapur como ejemplo para detallar las rutas de registro, requisitos aplicables y plazos.

- Requisitos previos y cronogramas para el registro de dispositivos médicos en los principales países del Sudeste Asiático: Incluye información sobre plazos, necesidad de registro en el país de origen, países de referencia, requisitos de certificación ISO 13485, etc., para Singapur, Malasia, Tailandia, entre otros.

- Rutas de registro regulatorio y estándares aplicables en Singapur: Como ruta completa, revisión inmediata, ruta acelerada, ruta simplificada, etc., así como situaciones y métodos de solicitud para aprobación prioritaria.

- Introducción a la ruta para importar dispositivos médicos no registrados en Singapur (SAR): En circunstancias específicas, se puede importar dispositivos médicos que no han pasado por el registro completo habitual mediante aprobación individual.

- Marco regulatorio y requisitos de LDT en Singapur: Los LDT no requieren evaluación ni registro, pero los laboratorios clínicos deben declarar, mantener documentación, cumplir con controles de producción y requisitos de supervisión post-comercialización.

- Rutas de dependencia entre Tailandia y Singapur: La FDA de Tailandia reconoce a la HSA de Singapur como institución de referencia, lo que puede acelerar el procedimiento de registro de dispositivos médicos, y ambas partes deben presentar documentos según lo estipulado.

5. Rutas de exportación de dispositivos médicos chinos al Sudeste Asiático e introducción a las regulaciones de cada país

- Rutas de exportación

- Modelo de distribuidor: La mayoría de las empresas lo adoptan inicialmente, utilizando redes de distribuidores para ingresar a mercados extranjeros, pero es necesario seleccionar buenos distribuidores y gestionar los riesgos de cooperación.

- Modelo de ensamblaje local/marca blanca: Adecuado para cumplir con requisitos específicos de países, necesidades de socios o planes de marca propios de la empresa, pero enfrenta desafíos de integración de la cadena de suministro y protección de propiedad intelectual.

- Modelo de establecimiento de fábrica local o adquisición de empresas locales: Adecuado para empresas grandes que desean profundizar en el mercado local, pueden gestionar la cadena de suministro y los canales de venta, pero deben considerar los riesgos de inversión y los costos de gestión.

- Regulaciones de cada país

- Indonesia: El registro de productos requiere designar un importador/distribuidor local para solicitar un permiso de circulación; algunos dispositivos médicos necesitan certificación halal; los distribuidores deben cumplir con las regulaciones pertinentes; existen requisitos de producción localizada y métodos de cálculo del contenido local; la inversión extranjera en producción y distribución de dispositivos médicos está completamente abierta, pero debe cumplir ciertas condiciones.

- Vietnam: La venta de dispositivos médicos importados debe cumplir condiciones de circulación; los requisitos de registro varían según la categoría del dispositivo médico; los distribuidores tienen regulaciones para la venta de algunos dispositivos médicos; se fomenta el uso de dispositivos médicos producidos localmente en hospitales públicos, y el contenido local puede determinarse según la definición de origen de las mercancías; la inversión extranjera tiene varias formas, cada una con regulaciones correspondientes.

- Singapur: La importación de dispositivos médicos requiere aprobación, y los fabricantes e importadores deben asumir responsabilidades correspondientes; se puede realizar producción y ensamblaje local mediante cooperación local, requiriendo acuerdos y conocimiento de los estándares de certificación; no hay restricciones para la inversión extranjera en empresas de producción y distribución de dispositivos médicos, pero deben cumplir ciertas condiciones.