1398

1398En el contexto de la reestructuración del comercio global y la constante evolución tecnológica, el mercado estadounidense, ese aparentemente conocido "viejo campo de batalla", está gestando silenciosamente nuevos cambios...

Fuente de la imagen: Internet

01/Gran mercado, entrada compleja

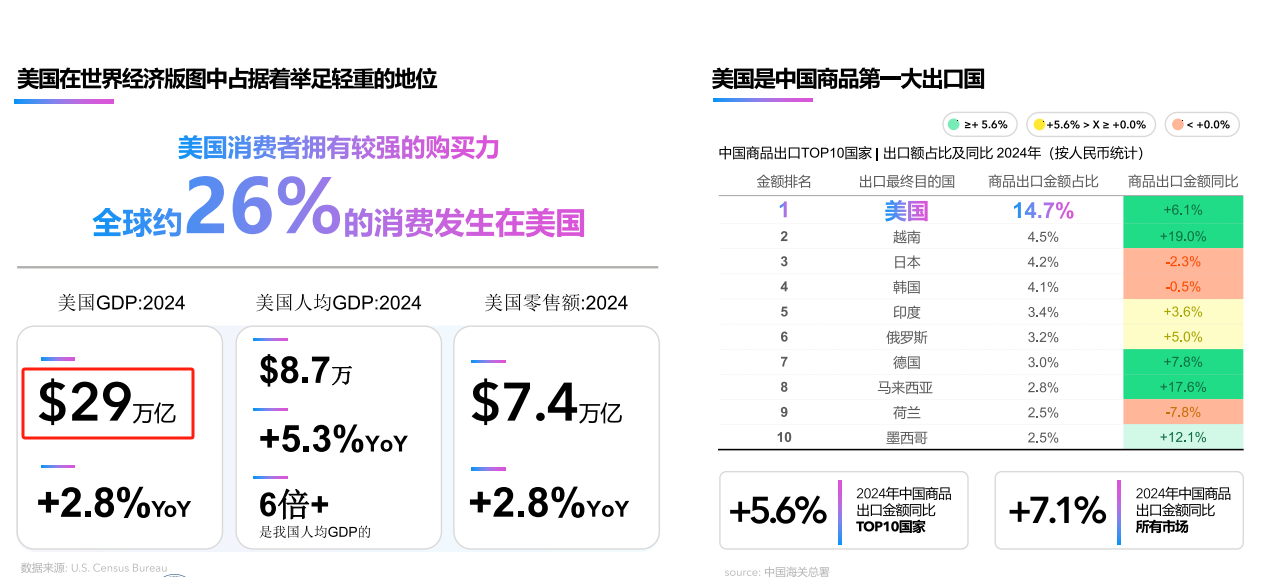

Según el "Libro Blanco de Tendencias del Mercado de Consumo de Electrónica de Consumo en EE. UU. 2025" publicado por Payoneer, en 2024, el PIB de EE. UU. alcanzó los 29 billones de dólares, con un PIB per cápita de 87.000 dólares, y las ventas minoristas totales sumaron 7,4 billones de dólares, consolidándose como el mercado de consumo más grande del mundo. En el sector de la electrónica de consumo, las ventas en EE. UU. fueron de aproximadamente 150 mil millones de dólares, ocupando el tercer lugar a nivel mundial, solo detrás de China y Europa.

Sin embargo, detrás de este enorme mercado también hay desafíos más severos. A partir de 2025, EE. UU. incrementó los aranceles a los equipos eléctricos/electrónicos fabricados en China al 145%, afectando también a categorías como maquinaria, muebles y equipos ópticos. Sumado a la incertidumbre política, la competitividad del producto por sí sola ya no es suficiente para que las marcas logren avanzar; se necesita mejorar la capacidad de respuesta ante la incertidumbre.

Fuente de la imagen: Payoneer "Libro Blanco de Tendencias del Mercado de Consumo de Electrónica de Consumo en EE. UU. 2025"

02/Reestructuración del consumo, surgen nuevas oportunidades

Al mismo tiempo, la estructura de consumo en el mercado estadounidense también se está reconfigurando silenciosamente, ofreciendo nuevos puntos de entrada para las marcas chinas. Entre ellos, la Generación Z y los adultos mayores se han convertido en los principales impulsores del consumo.

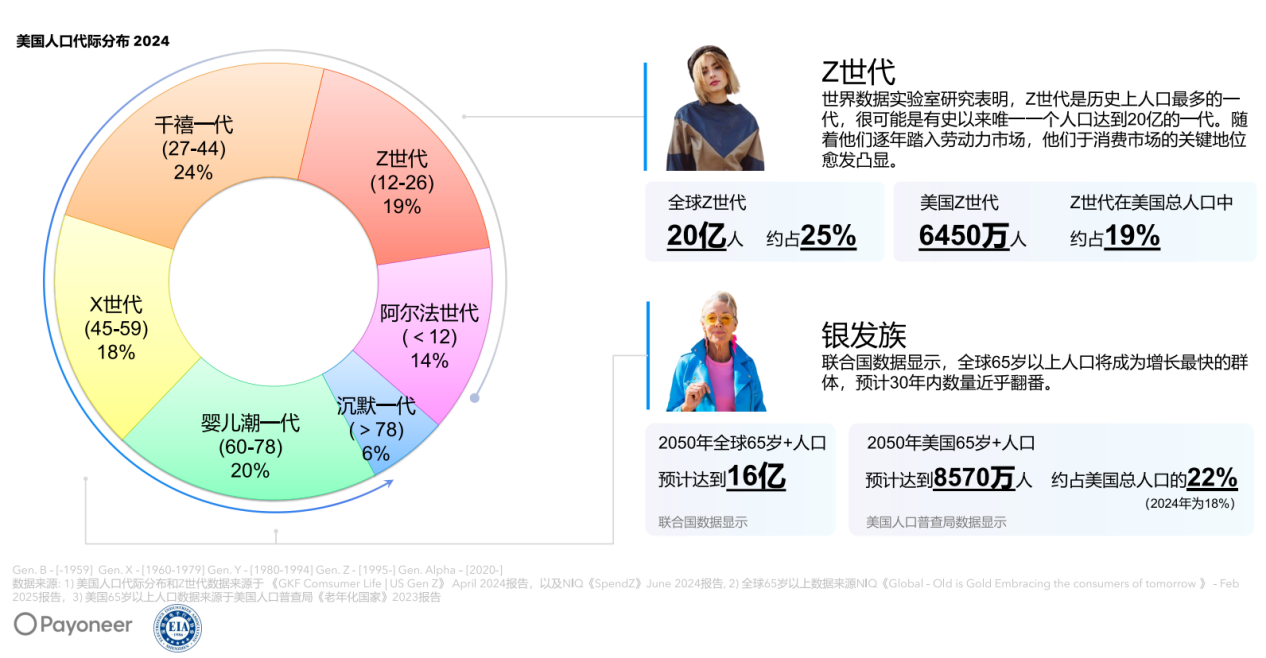

La Generación Z (de 18 a 26 años) representa el 19% de la población estadounidense y tiene una alta aceptación de las marcas chinas, valorando el diseño, la funcionalidad y la difusión social. El país de origen de la marca no es un factor determinante en sus decisiones.

Por otro lado, la proporción de adultos mayores en la población total también está en aumento, alcanzando el 18% en 2024 y se proyecta que llegue al 22% en 2050. Este grupo prioriza la salud, la comodidad y la conveniencia, y cuenta con un alto poder adquisitivo.

La convergencia de estos dos grupos está impulsando una nueva tendencia en los productos electrónicos de consumo hacia la inteligencia, la multifuncionalidad y la sostenibilidad ambiental.

Fuente de la imagen: Payoneer "Libro Blanco de Tendencias del Mercado de Consumo de Electrónica de Consumo en EE. UU. 2025"

03/La integración omnicanal se convierte en la nueva normalidad

Mientras se reconfigura la composición de los consumidores, la evolución de los canales de compra también está cambiando la forma en que las marcas se conectan con los usuarios. En 2024, las ventas online de electrónica de consumo en EE. UU. representaron casi el 60%, muy por encima del porcentaje total de ventas minoristas online (alrededor del 40%).

Además, aunque la cuota de los canales físicos ha disminuido, gigantes minoristas como Costco y Walmart mantienen una fuerte fidelidad gracias a sus sistemas de membresía, experiencias integrales y ventajas logísticas, especialmente entre los consumidores de mediana y tercera edad, para quienes la experiencia en tienda sigue siendo importante.

Al mismo tiempo, el rápido auge del comercio social lo ha convertido en un escenario de compra clave para grupos jóvenes como la Generación Z. Se informa que el GMV de TikTok Shop en el mercado estadounidense creció un 689% interanual, con un aumento de más del 100% en usuarios de pago diario. Entre los usuarios de 18 a 34 años, el 42% ya ha realizado compras a través de esta plataforma.

Fuente de la imagen: Payoneer "Libro Blanco de Tendencias del Mercado de Consumo de Electrónica de Consumo en EE. UU. 2025"

04/El camino de las marcas chinas para superar los desafíos

La continua evolución de la estructura de canales y las preferencias de los consumidores está impulsando un ajuste profundo de las estrategias de marca. Frente a la intensa competencia y las altas presiones regulatorias, las marcas chinas no se han quedado observando, sino que están buscando activamente cambios para encontrar puntos de ruptura.

Primero, la transición hacia productos inteligentes de alta gama, fortaleciendo la innovación. Los datos muestran que el 63% de los ingresos de la industria tecnológica de consumo global provienen de productos lanzados en los últimos dos años, y la Generación Z es un motor clave.

Segundo, la construcción de un nuevo sistema de cadena de suministro. Está surgiendo el modelo "China + N", que dispersa la capacidad de producción hacia el Sudeste Asiático o América del Norte para evitar barreras comerciales. Al mismo tiempo, se utilizan tecnologías como IA y blockchain para mejorar la eficiencia en la gestión del flujo de capital y el cumplimiento normativo.

Por ejemplo, Anker Innovations experimentó un crecimiento del 28% en las ventas de su plataforma propia y del 103% en las ventas de la plataforma Amazon en la primera mitad de 2024, resultado de la sinergia entre una distribución multicanal y la optimización de la cadena de suministro.

05/Conclusión

El mercado estadounidense está pasando de ser un simple escenario de ventas a convertirse en un "campo de pruebas de presión" para evaluar la capacidad de globalización de las empresas.

En el nuevo panorama comercial, la expansión internacional ya no consiste solo en vender productos, sino en competir en capacidades sistémicas, que incluyen un conjunto completo de mecanismos operativos globales: reconocimiento de marca, distribución de la cadena de suministro, innovación tecnológica, gestión de canales, comprensión cultural y cumplimiento normativo.

Creemos que solo las empresas con capacidad de "resistencia a largo plazo" podrán realmente arraigarse en el extranjero y lograr un crecimiento sostenible.