تم إعداد هذا التقرير من قبل معهد أبحاث السيارات الصيني، ويركز على تحليل تطور السيارات الصينية في السوق التايلاندية، ويتناول جوانب مثل الاقتصاد التايلاندي، واتجاهات سوق السيارات، وتوزيع العلامات التجارية الصينية، ورؤى المستهلكين، بهدف تقديم مرجع لتوسع شركات السيارات الصينية في السوق التايلاندية.

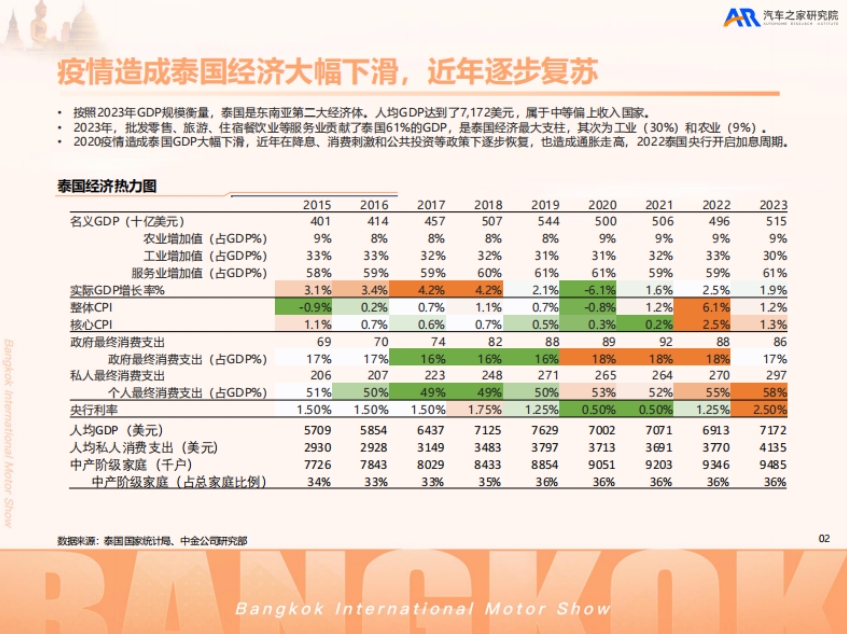

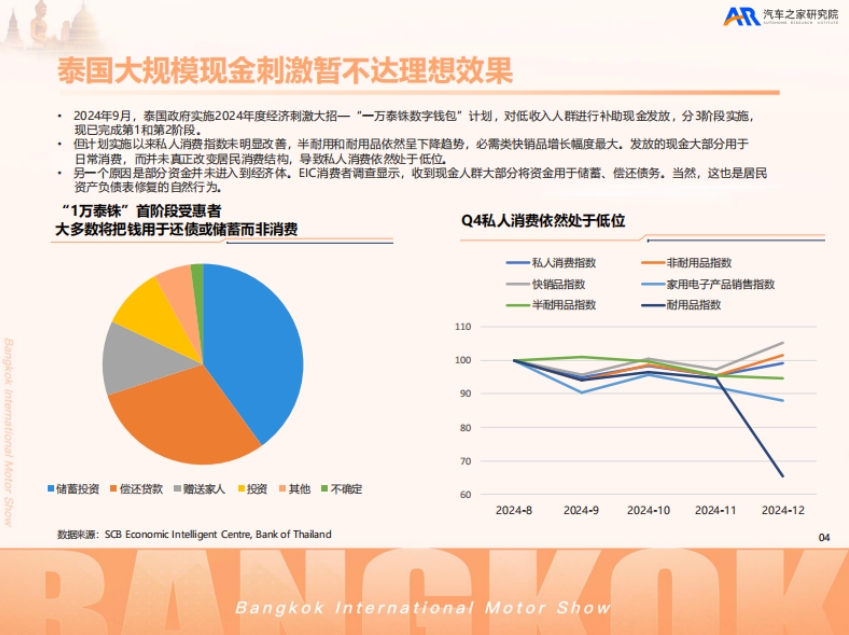

1. الوضع الاقتصادي والاستهلاكي في تايلاند: تايلاند هي ثاني أكبر اقتصاد في جنوب شرق آسيا، ويعتبر قطاع الخدمات الركيزة الأساسية للاقتصاد. تأثر الاقتصاد بجائحة كورونا وتراجع، ثم تعافى تدريجياً بفضل السياسات التحفيزية، لكنه يواجه أيضاً مشكلات التضخم ورفع أسعار الفائدة. التعافي الاقتصادي غير متوازن، حيث يُعد نمو الاستهلاك الخاص المحرك الرئيسي، لكن تأثير التحفيز النقدي الكبير كان محدوداً، كما يواجه التعافي تحديات مثل ارتفاع الديون الأسرية وتشديد الائتمان، مما أثر سلباً على سوق السيارات.

2. اتجاهات سوق السيارات في تايلاند: يعاني سوق السيارات التايلاندي حالياً من ضعف المبيعات بسبب ارتفاع تكاليف الاقتراض، وصعوبة الحصول على القروض، وانخفاض ثقة المستهلكين، وحروب الأسعار. على المدى المتوسط والطويل، من المتوقع أن يتعافى السوق بفضل دعم السياسات الحكومية للكهربة، معتمداً على السيارات الكهربائية. من حيث هيكل السوق، انخفضت حصة الشاحنات الصغيرة التقليدية، بينما ارتفعت حصة سيارات الدفع الرباعي (SUV)، وتباطأ نمو معدل انتشار الطاقة الجديدة. تطورت العلامات التجارية الصينية بسرعة، متجاوزة العلامات الأمريكية في حصة السوق، وأصبحت الخيار الأول للمستهلكين التايلانديين في سوق الطاقة الجديدة.

3. تحليل توزيع العلامات التجارية الصينية: تسارعت العديد من شركات السيارات الصينية في التوسع في السوق التايلاندية، حيث انتقلت من التصدير الكامل للسيارات في المراحل المبكرة إلى إنشاء مصانع محلية وتعميق سلسلة الصناعة بأكملها. تعزز هذه الشركات قدرتها التنافسية من خلال بناء المصانع وإطلاق منتجات جديدة، مثل BYD وGAC Aion اللتين حققتا نمواً ملحوظاً في المبيعات، لكنها تواجه أيضاً تحديات مثل مراقبة الجودة والتوطين.

4. رؤى المستهلكين التايلانديين: 72% من المستهلكين التايلانديين مستعدون لشراء سيارات من العلامات التجارية الصينية، والسبب الرئيسي هو انخفاض أسعار السيارات الصينية وتكاليف استخدامها، مما يلبي احتياجات المستهلكين من حيث القيمة مقابل المال، والوظائف العملية، والذكاء، والأناقة. على الرغم من أن السيارات التقليدية التي تعمل بالوقود لا تزال الخيار السائد، إلا أن معظم المستهلكين لديهم معرفة معينة بالعلامات التجارية الصينية للسيارات ذات الطاقة الجديدة.

5. الخلاصة والتوقعات: يتمتع سوق السيارات التايلاندي بإمكانيات كبيرة، حيث تمثل السياسات الداعمة، وسلسلة الصناعة المتكاملة، وارتفاع قبول المستهلكين للطاقة الجديدة فرصاً. ومع ذلك، يواجه تحديات مثل المنافسة من الشركات اليابانية، ونقص التوطين، والحاجة إلى تحسين سمعة العلامات التجارية. يمكن للعلامات التجارية الصينية تجاوز عقبات التطور من خلال توسيع السوق، وابتكار الخدمات، وتحسين سلسلة الصناعة، وتعزيز الابتكار التكنولوجي.