"2024 Southeast Asia Going Global Research Report: Macroeconomic Section" focuses on the current development trends of Southeast Asia's economy and the specific models of China's participation in the Southeast Asian economy. The main contents are as follows:

1. Current Status of Southeast Asian Economy

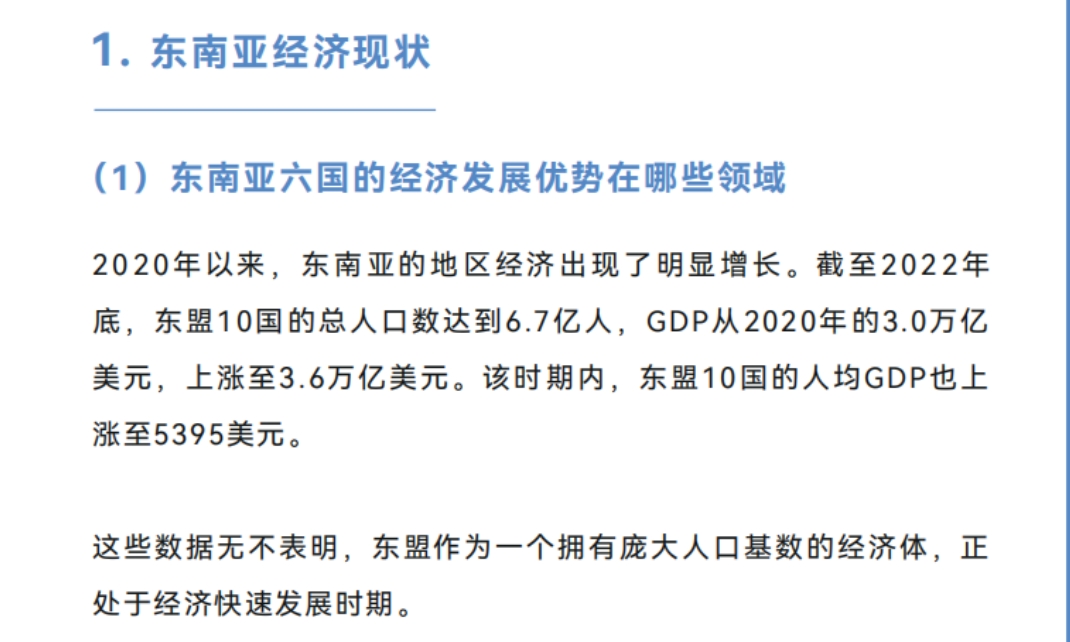

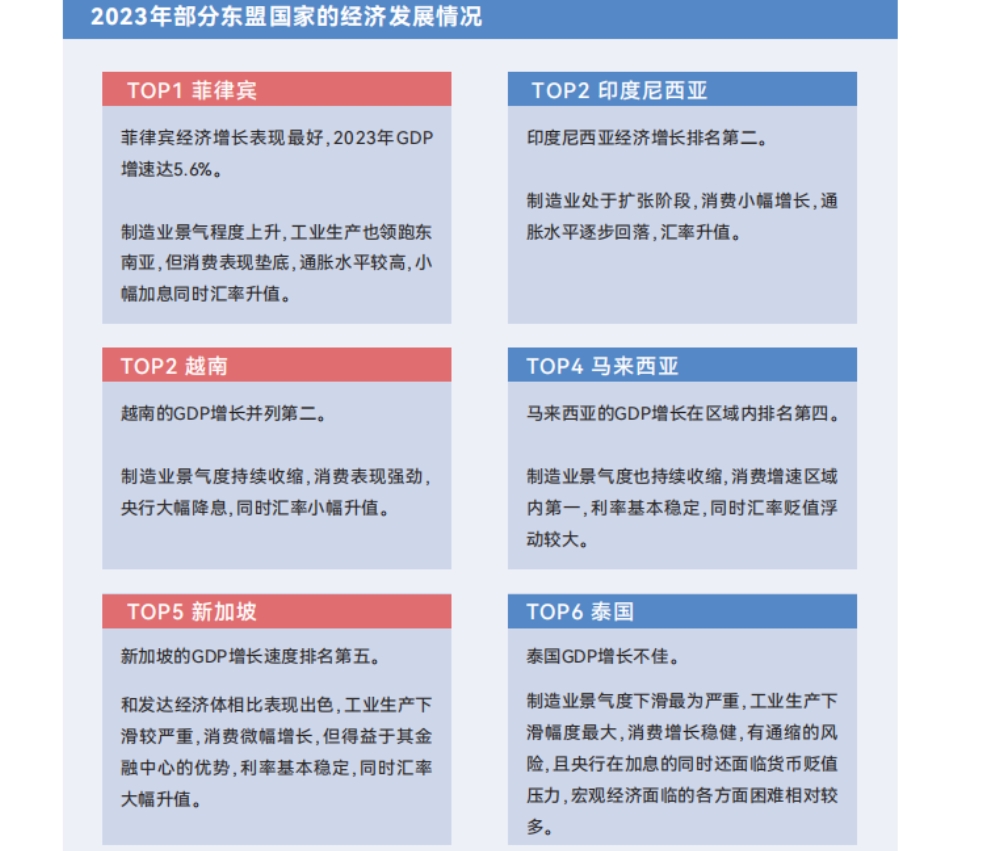

- Economic Development Advantage Areas: From 2020 to 2022, ASEAN's economic growth was significant, with GDP rising from $3.0 trillion to $3.6 trillion, and per capita GDP also increasing. In 2024, overall growth is expected to reach 4.9%, with some countries exceeding 6%. Economic growth advantages include domestic consumption, tourism, demographic dividend, trade, and inflow of foreign direct investment. Different countries have varying performances in manufacturing and consumption, such as the Philippines experiencing an upturn in manufacturing but lagging in consumption, while Vietnam shows strong consumption but contraction in manufacturing.

- Challenges Faced

- Growth Momentum Under Pressure: High consumption growth may be difficult to sustain, exports are declining, manufacturing is under pressure, investment enthusiasm is cooling, and the scale of FDI inflow is decreasing.

- Obstacles to Inflation Decline: Rising energy and food prices have brought inflation, which, although has eased, still poses pressure. At the same time, there is a need to balance fighting inflation with economic recovery, as well as debt and fiscal stimulus.

- Weakening Demographic Dividend: Most countries have relatively ideal population structures, but some face issues such as aging, high unemployment rates, and low labor productivity.

- High Financial Dependence: Financial markets are influenced by monetary policies of central banks in developed economies, with net outflows from stock and bond markets, and foreign exchange markets experiencing relative depreciation against the US dollar.

2. How China Participates in the Southeast Asian Economy

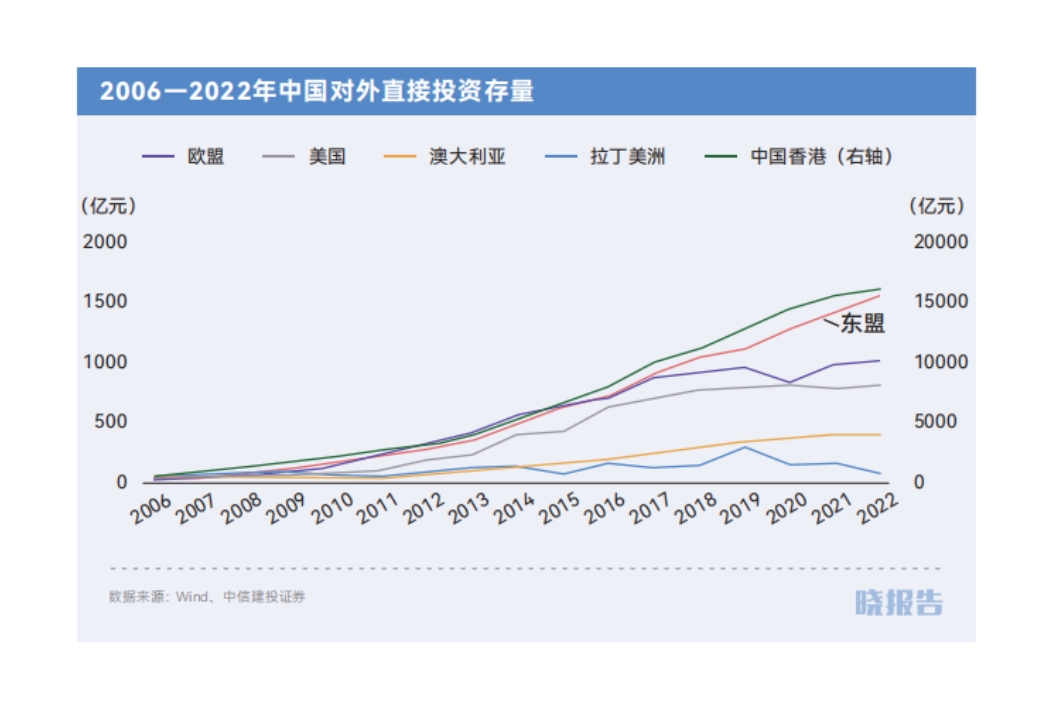

- Investment Overview: Following China-US trade frictions and post-pandemic supply chain "de-risking," China's industrial chains have moved outward, with a large amount of capacity shifting to Southeast Asia since 2017. As of 2022, China's investment stock in eight ASEAN countries varies, with Indonesia receiving the largest stock. There are mainly two investment models, with direct investment and FDI proportions in Indonesia, Malaysia, Thailand, and Vietnam on the rise, suggesting the first model (building new factories or assembly plants overseas). Investment covers a wide range of industries, with manufacturing accounting for the largest and fastest-growing share.

- Southeast Asia's Advantageous Industries and China's Investment Focus

- Vietnam: Mainly electronics, with parts of China's textile, apparel, footwear industry chains and low value-added segments of consumer electronics shifting to Vietnam.

- Indonesia: Mainly minerals, with Chinese companies investing in metal mining and processing, opening up the channel from nickel mining to new energy raw materials, and car companies also investing and laying out in Indonesia.

- Malaysia: Mainly services, with a large Chinese diaspora attracting Chinese brand investments. Manufacturing FDI flows into industries such as electrical equipment, and Chinese companies invest in packaging and testing plants, photovoltaic industry, and automotive industry in Malaysia.

- Thailand: Mainly manufacturing, with China investing heavily in metal products and other industries. Companies like Midea and Haier invest in the air conditioning industry in Thailand, and Chinese car companies are also laying out the new energy vehicle sector in Thailand.

- Laos: Mainly infrastructure, with China being the largest investor in Laos, covering a wide range of fields and assisting in agricultural and infrastructure construction, as well as cross-border industrial cooperation and emerging fields.

3. Future Opportunities for China's Participation in Southeast Asian Economic Development

- Four Models for Enterprises Going Global: Export trade (exporting products or services via overseas trade partners), overseas marketing (building overseas sales and marketing teams to enhance brand awareness), overseas operations (developing localized operational capabilities overseas with a complete physical business operation system), and globalized operations (having global templates and operational control systems to form a global ecosystem of cooperation and synergy).

- Pain Points for Enterprises Participating in Southeast Asian Investment: Multiple risks (complex policies and regulations, high market uncertainty), management difficulties (large cultural differences, poor communication), significant differences (difficulty integrating management systems after acquisitions), poor resilience (new requirements for supply chain flexibility and resilience), as well as specific issues in risk control compliance, global management and operations, talent and organization. Other challenges include insufficient understanding of local markets, lack of channel resources and ecosystem partners, lack of technical infrastructure and relevant talent, and ESG requirements.