2642

2642La carte mondiale de TikTok Shop s'agrandit avec une nouvelle destination : le marché japonais.

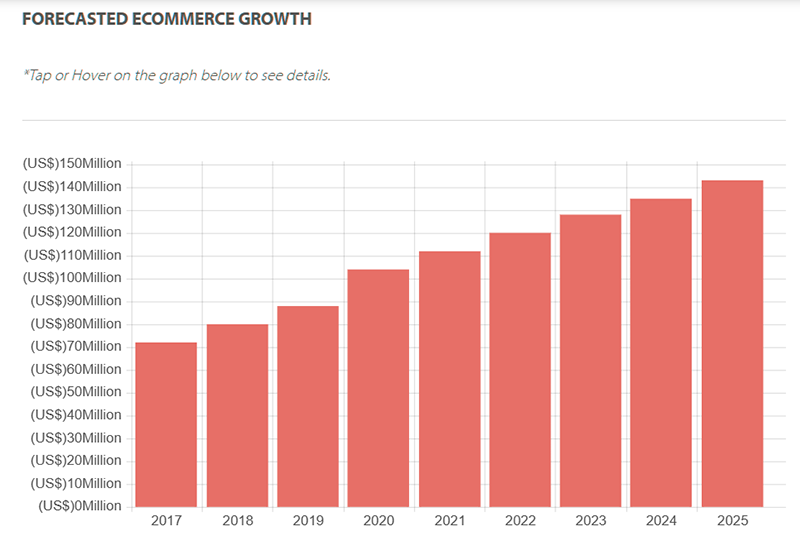

Selon des informations officielles, la plateforme sera officiellement lancée en juin 2025, avec un premier recrutement de vendeurs locaux, pour dynamiser le marché du commerce électronique japonais via le modèle « vidéo courte + live streaming ». Cette initiative est motivée à la fois par l'attrait d'un marché japonais du e-commerce estimé à 206,8 milliards de dollars (prévision 2025) et par le potentiel de croissance d'un taux de pénétration du live shopping inférieur à 5 %.

Cependant, ce marché en apparence « juteux » cache en réalité des défis « coriaces ».

Source : Nikkei

Opportunités de marché : utilisateurs à forte valeur ajoutée et dividendes structurels

Le Japon est le troisième plus grand marché de e-commerce au monde. En 2023, le volume des transactions a dépassé 22 000 milliards de yens (environ 1 100 milliards de yuans), et il devrait atteindre 206,8 milliards de dollars en 2025. En contraste frappant avec la taille de ce marché se trouve son « caractère traditionnel » en matière de commerce électronique : le taux de pénétration du live shopping est inférieur à 5 %, bien loin des 20 % de la Chine et des 15 % des États-Unis. Cette contradiction constitue précisément le point d'entrée idéal pour TikTok : en utilisant le modèle du « commerce d'intérêt » combinant « vidéo courte + recommandation algorithmique + live », il s'agit de stimuler le potentiel de croissance des consommateurs japonais, les faisant passer d'un « achat par recherche » à un « achat par découverte ».

Source : Internet

En termes de base d'utilisateurs, TikTok compte plus de 26 millions d'utilisateurs actifs mensuels au Japon, dont plus de 60 % ont entre 18 et 34 ans, et le temps d'utilisation quotidien moyen dépasse 60 minutes. Ce groupe est de plus en plus réceptif à l'idée que « le contenu est un achat » : 42 % des utilisateurs japonais admettent avoir eu une impulsion d'achat après avoir vu une vidéo courte, avec une forte demande pour les catégories comme les cosmétiques, les marques de mode et la décoration intérieure. Plus crucial encore, le panier moyen du e-commerce japonais reste élevé, avec une transaction moyenne pour l'habillement atteignant 8 000 yens (environ 400 yuans), soit 2,3 fois celui du marché chinois. Cela signifie que même une légère augmentation du taux de pénétration peut libérer un potentiel de GMV considérable.

Source : Internet

Les « os durs » de la réalité : barrières culturelles et siège des géants

Cependant, la spécificité du marché japonais en fait l'un des champs de bataille du e-commerce les plus difficiles à conquérir au monde. Le premier défi vient de la culture de consommation : les consommateurs japonais sont réputés pour être « pointilleux sur les détails », avec un taux de retour historiquement plus élevé que sur les marchés occidentaux. Le taux de retour pour l'habillement atteint 15 à 20 % (3 fois celui du marché de l'Asie du Sud-Est), ce qui impose des exigences strictes en matière de gestion de la chaîne d'approvisionnement et de coûts d'exécution. Plus délicat encore est le « sens du rituel » dans la psychologie de consommation : les utilisateurs japonais apprécient l'expérience raffinée du processus de sélection, plutôt que le plaisir immédiat des « 9,9 yuans avec livraison gratuite » en Chine. Si TikTok copie aveuglément la stratégie de bas prix, il risque de nuire à la prime de marque et de tomber dans le piège de « gagner du trafic sans faire de profit ».

Source : Internet

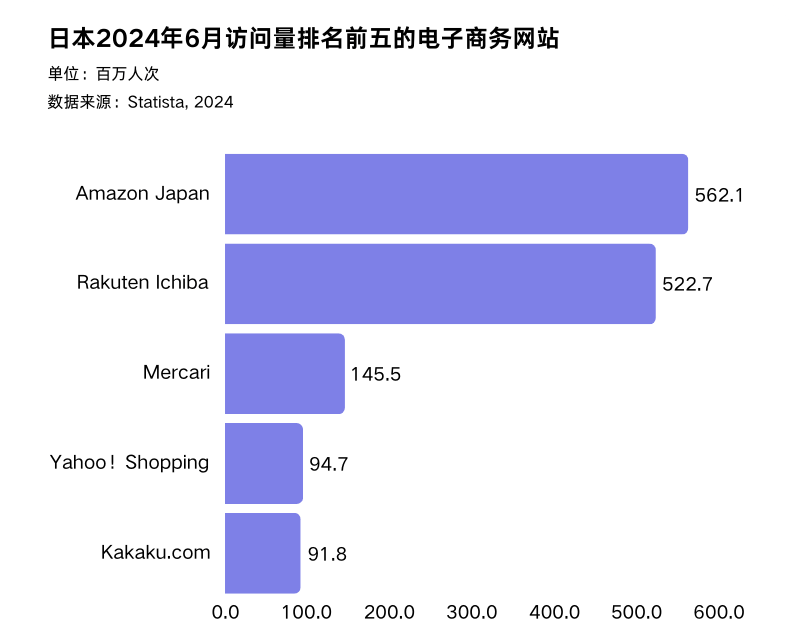

Le deuxième défi vient du paysage concurrentiel. Rakuten et Amazon Japan détiennent plus de 70 % des parts de marché, ayant déjà construit un réseau logistique complet (Rakuten assure une livraison le lendemain dans 98 % du pays), un système de paiement (Rakuten Pay compte plus de 40 millions d'utilisateurs) et un écosystème d'adhésion. Pour percer, TikTok doit « frapper plus fort » en matière d'opérations localisées : par exemple, collaborer avec des agences MCN locales pour incubateurs des influenceurs de niche, en se concentrant sur des industries clés comme les cosmétiques et l'anime ; ou lancer des « ventes flash limitées » et des « réductions exclusives des streamers » pour renforcer la perception de bas prix. Cependant, pour l'instant, sa logistique repose encore sur l'expédition directe transfrontalière et des prestataires de services tiers, et la construction d'entrepôts locaux n'a pas encore été déployée, ce qui pourrait entraîner des délais d'exécution inférieurs à ceux de ses concurrents.

Source : Internet

Conclusion : un jeu à long terme entre risque et récompense

L'entrée de TikTok Shop au Japon est fondamentalement une aventure à « haut investissement, haut rendement ». Pour les vendeurs, la capacité à conquérir cet « os dur » dépend de trois compétences clés : la rationalisation de la chaîne d'approvisionnement (contrôle de la qualité), la profondeur des opérations localisées (adaptation culturelle) et la flexibilité du contrôle des coûts (logistique et gestion des retours). À court terme, les premiers entrants devront supporter les coûts d'expérimentation ; à long terme, les gagnants construiront des barrières concurrentielles difficiles à reproduire.